Financial security is something that’s an illusion in this current economic climate. Economic instability is often seen as a major obstacle to job security.

Once the safety net of job security breaks, one needs a concrete plan to restructure their financial position.

Tools that manage your finances before you begin spending are crucial for paying bills on time. Even when you have a job or business that pays all the bills, it’s important to ensure that there are tools in place to help with cash flow management.

Economic instability results in layoffs and a major shift in the AI bubble.

There are no safe jobs. The recent Amazon layoffs show that even the biggest tech companies cannot guarantee employment security.

No one could have predicted Shell’s divestment plans from South Africa. And seeing numerous Nestlé products in grocery stores doesn’t lessen the blow of the global layoffs.

When the salary is no longer available, you must change your lifestyle. It can help prevent asset repossessions. Repossessions are emotionally painful. Being honest with what has to be done after a loss of income can take time. Expenses have to be reduced.

When total expenses are reasonable, relative to income, there are better savings and investment opportunities. In the event of layoffs or loss of income due to unfavorable business conditions, you can use the money saved or invested to pay essential expenses.

Transitions are unpredictable.

No one can predict the job market with certainty. Amazon is a big player in the AI movement. The software engineers who were laid off surely didn’t see it coming. It’s a reminder that no company or entity can be too big to fail.

Being flexible is a prerequisite. Translators have to pivot in the world of AI tools that can translate with 100% accuracy.

Human behavior changes.

When human behavior changes, spending habits change as well. Things that were once a necessity can be changed. A monolithic approach to business, building, and how you live fails.

Estate living changes from being a place of safety and security to a financial burden with exorbitant levies and rates. Most emergency funds cannot cover such expenses for long periods.

Maslow’s Hierarchy of Needs fails to account for the unpredictable nature of human behavior in relation to access to monetary funds. Therefore, safety needs can be destroyed by unforeseen circumstances.

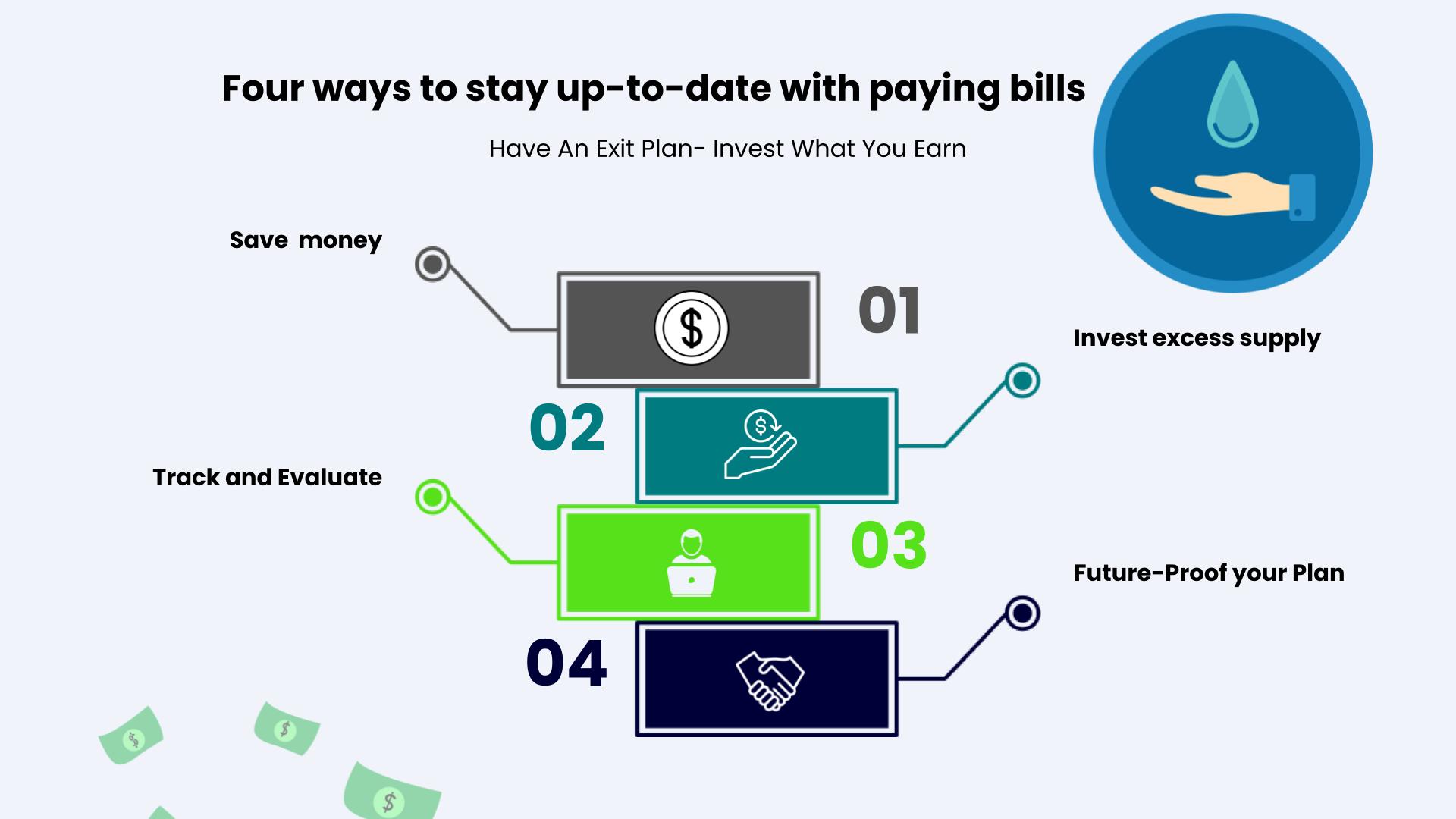

Four ways to stay up-to-date with paying bills.

Have An Exit Plan- Invest What You Earn.

1. Save money.

Saving more money helps with paying bills when income is scarce.

2. Invest your excess supply.

Investing money in various investments can grow your money to the point that you can cover your bills with dividends earned, share growth, or appreciation of assets.

3. Track and evaluate your spending.

Cut wasteful expenses by tracking your bills. For example, eliminate subscriptions and unused gym memberships.

4. Future-Proof your Plan.

God knows times of abundance and lack. Wise counsel, like in the days of Joseph, is needed. Genesis chapter 41.

Leverage Savings by Diversifying.

Use multiple high-interest-yielding bank accounts.

Interest earned can cover bills like levies and electricity.

Save across multiple banks to get the best savings products.

Don’t be afraid to shop outside your own bank for the best savings interest rates. And should your own bank fail, you can get access to up to 100,000 rands as per the Corporation for Deposit Insurance (CODI), which is South Africa’s Deposit Insurance Scheme.

For example, if you bank with ABC Bank and it closes down. If you have 500,000 rands, only the first 100,000 rands can be repaid to you immediately until the liquidation process is completed. Therefore, placing a large sum of money in one bank is not wise.

Diversify and ensure that you have short-term savings accounts without a long waiting process to access funds in case of an emergency. And place money that you won’t need within twelve months into a high-interest-yielding savings account.

Leverage investments by allowing compounding to do its work.

Investing consistently over a long period yields greater benefits.

Optimize tax-free savings accounts for long-term investments through Exchange-Traded Funds (ETFs) to yield greater compounding effects and minimize risk. All the money you won’t need until retirement should go into this section. Ensure that you don’t exceed the tax-free yearly or lifetime limit, as it constantly changes per the Finance Minister’s recommendations. The 46,000 rands saved in your tax-free brokerage account can make you a multimillionaire by the time you retire.

Consider investing in commodities such as silver and gold to protect yourself against inflation. Also invest in mining companies that produce commodities that can not be easily stored through private storage, by buying shares. For example, invest in companies that produce crude oil or copper.

Educate yourself about alternative investments, such as cryptocurrency, and check whether centralized crypto platforms are registered as authorized Financial Service Providers, before investing. Financial education is a long-term process that is constantly evolving; you cannot leave your financial education in someone else’s hands, even if you have someone qualified to invest on your behalf.

Track and evaluate performance.

Once you have established your weaknesses, it’s much easier to make the necessary changes.

Use financial tools to help with your spending habits, savings, and investment goals.

Pay off high-interest debt before you start long-term savings and investments. Do a monthly check-in, and see how you are moving along with canceling unused subscriptions and cutting out luxury spending. Do a quarterly, half-year, and year-end personal financial audit and make the necessary changes based on the data presented.

Set your financial freedom number, once you have more than enough to cover your living expenses. This will motivate you to keep going.

God’s plans always supersede our own plans.

With South Africa’s high unemployment rate, we have to consider that others are struggling to find work or sustain a business. How does one leverage what they have to survive? One has to use what they have within their homes and the talents that they possess by coming up with creative solutions.

‘To one he gave five talents, to another two, to another one, to each according to his ability. Then he went away.’ Matthew 25:15

The widow took the little that she had in her home to start an olive oil business to pay off creditors, before they took her two sons into slavery.

‘Elisha replied to her, “How can I help you? Tell me, what do you have in your house?”

“Your servant has nothing there at all,” she said, “except a small jar of olive oil.”’ 2 Kings 4:2

Using one’s talent to further our lives is another way to overcome struggles. The one who has the least cannot bury their talent because of fear of failure, but must use what God has given them.

‘But he who had received the one talent went and dug in the ground and hid his master’s money.’ Matthew 25:18

Even when the margin of success is little, one cannot remain idle. Resources gathered by little add up to a lot when they are put together.

‘Elisha said, “Go around and ask all your neighbors for empty jars. Don’t ask for just a few.’ 2 Kings 4:3

Compounding can surpass what you didn’t foresee through your own lens. Just cutting one thing to save for your future can help you to be in a better financial position decades later.

Joseph’s preparation brought his family together through a time of famine and great adversity. He was Pharaoh’s right-hand man with the ability to know the times in a world where others saw no need to save extra grain for the seven lean years they had to overcome. The future is unpredictable; therefore, one needs to stay ahead of what is happening by hearing God’s word regarding all things.

Disclaimer: Upper Ground is not liable for any financial decisions you make. Consult a certified financial professional for financial services.

Pingback: Minimalism can teach you to be financially resourceful - Upper Ground